New Report Details the $76 Billion U.S. Waste Industry

Date: January 5, 2020

Source: Waste Business Journal

New Report Details the $76 Billion U.S. Waste Industry

Waste Market Overview & Outlook 2019

With all the bad news focused on the trouble with recycling it's easy to overlook

the overall strength of the U.S. waste management industry which grew

by nearly 4 percent last year to $76 billion. Waste

Business Journal's 363-page report: The Waste

Market Overview & Outlook 2019 details the industry, its business

segments, key market participants, and how they interact with one another

and the overall economy.

With all the bad news focused on the trouble with recycling it's easy to overlook

the overall strength of the U.S. waste management industry which grew

by nearly 4 percent last year to $76 billion. Waste

Business Journal's 363-page report: The Waste

Market Overview & Outlook 2019 details the industry, its business

segments, key market participants, and how they interact with one another

and the overall economy.

Purchase the Waste Market Overview & Outlook 2019 (363 pages) for $995.

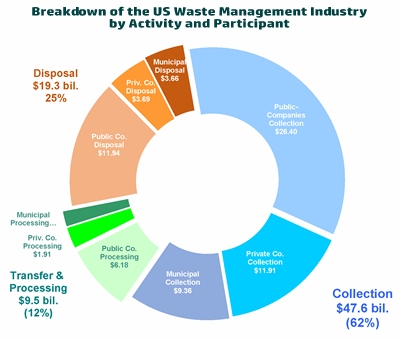

Last year the trend towards increasing privatization continued as publicly-traded companies accounted for 60 percent of industry revenues. That is up from less than 50 percent in the early 90s when municipalities accounted for 35 percent of revenues. Municipalities account for just 19 percent today. The business of waste is 62 percent collection, 12 percent recycling and transfer, and 25 percent disposal, which includes landfilling and to a much lesser extent, waste-to-energy.

Components of the Waste Stream

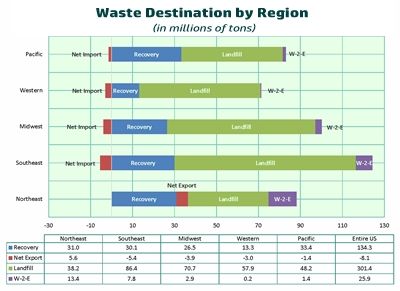

The report details with historical and projected statistics of four primary non-hazardous waste streams: municipal solid waste (MSW), organic wastes, construction and demolition debris (C&D) and non-hazardous industrial and special wastes. The report estimates that the U.S. generated 456 million tons, or 7.6 pounds per person of MSW last year. This figure is significantly more than U.S. EPA estimates, but Waste Business Journal figures are based on individual facility surveys of every waste processing and disposal operation across the country. That includes landfills, transfer stations, recycling facilities, waste-to-energy plants, composting operations and more.

Of that 456 million tons of MSW, we recycled (or composted) 29 percent leaving 301 million tons (66 percent) that was landfilled and 8 million tons (6 percent) that was burned for energy recovery. The U.S. imported 8 million tons from other countries, mostly Canada. Publicly-traded companies handled 58 percent of total landfill volumes, while private companies accounted for 14 percent and municipally owned landfills 28 percent.

Pricing Increases…Companies Share the Added Costs of Recycling with Customers

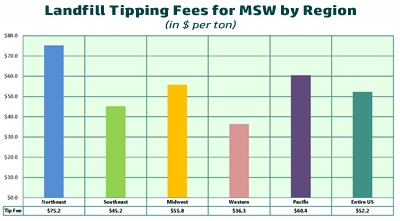

Meanwhile, landfill tipping fees have grown steadily over the years in line with inflation, growing demand for disposal amid fewer landfills and because the big firms have exercised more pricing discipline in recent years by avoiding costly battles over market share. The national average tipping fee for 2018 was $52.20, up from $32.90 in 1998. WTE tip fees showed slightly more variability over the 20-year timeframe. Tipping fees vary widely be region and in accordance with the availability of landfill capacity amidst population density and demand for disposal. Prices have risen faster in the Midwest and southeast as waste is exported to these regions from the Northeast.

Increased Efficiencies through Vertical Integration

Recent mergers including Waste Management's proposed takeover of Advanced Disposal, promises a reshaped industry much further along its path of privatization and concentration. The companies understand that one way to deal with turbulent economic times amidst rising fuel, labor and equipment costs is to streamline operations and vertically integrate their markets. Integrated companies can better utilize their landfills by controlling a greater percentage of surrounding collection assets.

Landfill Capacity Expected to Contract Further…Especially in the Northeast

Landfills themselves are becoming more important as old sites close, demand for disposal steadily climbs, accelerated by recycled materials sent there that have been collected but have no market since China imposed much more stringent requirements. Consequently, remaining landfill capacity which has hovered around 20 years for the last decade, is expected to shrink to just 17 years by 2022. Landfill capacity is especially critical in the Northeast where capacity is expected to shrink to less than 10 years by that time.

Renewed Focus on Hedging Costs

Rising costs have focused company managers on disciplined price increases especially now that the industry is more consolidated, making them more attentive to return on invested capital, more rational about valuing existing landfill capacity and mindful of lessons in the past when pricing was sacrificed.

Past volatility of fuel costs and recent volatility in recycled commodity prices have led waste firms to share those increases with customers by adding surcharges to their contracts. Expect to see continued focus on controlling vehicle maintenance and insurance costs while investing in fleet upgrades and worker safety programs. Additional cash from operations will likely go towards "tuck-in" acquisitions, asset swaps and other vertical integration measures for which companies can reap immediate cost savings.

Relatively low natural gas prices together with a growing infrastructure of fueling facilities is leading companies and municipalities to invest in converting their fleets to compressed natural gas (CNG) and liquefied natural gas (LNG) powered vehicles. Other benefits including lower emissions and quieter engines makes the fleets more welcome to the communities they serve. While helping the collection profitability, low natural gas prices are hurting the waste-to-energy business. Only one new mass burn plant has been built since 1995 and many waste conversion plants proposing to use advanced technologies have either been discontinued, cancelled or put on hold.

Other Segments and Waste Streams Covered:

- Construction and Demolition Debris Generation, Recovery and Disposal

- The growing problem of E-Waste, Legislation, Processors and Solutions

- Renewed focus on Organics and new Food Waste Programs

- Scrap Tires, Recycling and Conversion to Energy

- Waste Industry Equipment, Manufacturers and Segments

And much more…

Comprehensive Dataset Included

Included with this comprehensive and detailed 363-page report is an Excel dataset that includes historical and projected data on waste generation, recovery, exports, and disposal by landfill or WTE, remaining capacity and tipping fees for each major category of waste. The waste streams are broken out by MSW, organics, C&D, and industrial wastes. The statistics are aggregated by state, region and for the entire U.S.

To learn more about the Waste Market Overview & Outlook 2019 (363 pages), which costs $995 US, visit: www.wasteinfo.com/overview.htm. Or, call (619) 793-5190.

Sign up to receive our free Weekly News Bulletin