Casella Net Income Rises 22% on Pricing

Date: October 29, 2020

Source: Casella Waste Systems, Inc.

Casella reported healthy third quarter revenues and earnings that improved with recovering economic and construction activity. Net income rose to $15 million, $0.31 per share versus $12 million, $0.26 per share a year ago. Revenues were also up because of recent acquisitions, core price increases, and higher recycling volume and revenues. Overall pricing improved 4 percent, with collection pricing up 3.7% and landfill pricing up 6.9 percent.

The company said it acquired nine companies worth $21 million in annual revenue so far this year and reported recycling revenue of $12.76 million, up 18.9 percent year-over-year due to higher commodity values, and ongoing interest in resource solution services. Company CFO Ned Coletta estimated that 65 percent of the commercial and industrial collection revenue affected by suspensions had returned, with another 10 percent expected to come back as seasonal winter businesses start up.

The company reinstated annual adjusted free cash flow targets to pre-pandemic levels, citing better than expected results, and is now aiming for $60-65 million and has raised annual revenue guidance to $760-775 million.

PRESS RELEASE

Casella Waste Systems, Inc. Announces Third Quarter Results; And Raises Fiscal Year 2020 Guidance

— Financial results exceeded expectations, with strong operating execution, real-time cost controls and disciplined cash flow management.

Highlights for the Quarter and Year-To-Date Ended

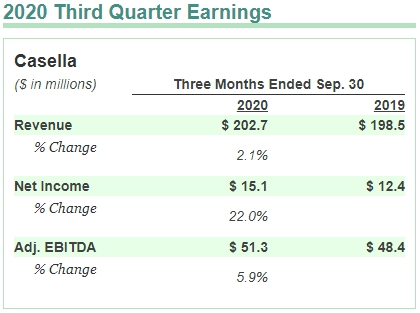

- Revenues were

$202.7 million for the quarter, up$4.1 million , or up 2.1%, from the same period in 2019. - Overall solid waste pricing for the quarter was up 4.0%, with collection pricing up 3.7%, and landfill pricing up 6.9%, from the same period in 2019.

- Net income was

$15.1 million for the quarter, up$2.7 million , or up 22.0%, from the same period in 2019. - Adjusted EBITDA, a non-GAAP measure, was

$51.3 million for the quarter, up$2.8 million , or up 5.9%, from the same period in 2019. - Net cash provided by operating activities was

$111.9 million for the year-to-date period, up$40.4 million , or up 56.5% from the same period in 2019. - Adjusted Free Cash Flow, a non-GAAP measure, was

$60.0 million for the year-to-date period, up$35.9 million from the same period in 2019. - The Company raises its revenue, net income, Adjusted EBITDA, net

cash provided by operating activities, and Adjusted Free Cash Flow guidance

ranges, for the fiscal year ending

December 31, 2020 ("fiscal year 2020"). The Adjusted Free Cash Flow range is raised to the original level set in February for fiscal year 2020 despite the headwinds associated with the COVID-19 pandemic.

"I remain extremely proud of our 2,500 dedicated employees, especially our

frontline team members who have worked hard during this challenging time to

effectively service our customers while maintaining our high safety and environmental

standards," said

"Solid waste volumes were down (8.4%) year-over-year in the quarter, as certain customers sustained negative business impacts from the COVID-19 pandemic," Casella said. "Volume declines continued to moderate throughout the quarter as various commercial customers reopened or increased services, construction projects resumed, and overall building activity increased; and overall economic activity rebounded across our mainly secondary and rural markets in the northeast. Given these sequential improvements, by September our solid waste volumes were down (4.8%) year-over-year for the month."

"Despite these volume headwinds and roughly

"Systems enhancements over the last year have improved our ability to analyze and respond to key sales trends and operational metrics in a more responsive and intelligent manner," Casella said. "This visibility coupled with our collaborative efforts to reset customers' service levels to their actual needs during the pandemic has allowed us to proactively scale operations to lower volumes, driving costs quickly out of the business."

"We continue to execute well against our long-term growth strategy and year-to-date

through October we have acquired nine businesses with approximately

For the quarter, revenues were

Net income was

Operating income was

For the year-to-date period, revenues were

Net income was

2020 Outlook

"Given our strong execution during the third quarter, combined with increased visibility of the negative volume and cost impacts of the COVID-19 pandemic, we are raising our financial guidance ranges for fiscal year 2020," Casella said. "There are still many variables outside of our control, such as new waves of COVID-19, additional stay-at-home orders and impacts on the economy as the Federal stimulus programs run their course. However, our team has remained nimble in this rapidly changing environment and continues to flex operating costs and drive operating efficiencies to offset lower volumes or other headwinds."

"Despite the enormous challenges presented in 2020 due to the COVID-19 pandemic, we are immensely proud to raise our Adjusted Free Cash Flow guidance range back to the same range as first established in February," Casella said. "This is a true testament to the hard work and dedication of our team, the resiliency of our business model, and our asset positioning in the disposal capacity constrained northeast market."

"Our guidance ranges assume a modestly declining to stable economic environment for the remainder of the year," Casella said. "And the guidance ranges do not contemplate a severe relapse of the COVID-19 pandemic or new stay-at-home orders, which may negatively impact commercial and general economic activity in our markets through the remainder of 2020."

The Company updated guidance for fiscal year 2020 by estimating results in

the following ranges (as compared to the guidance ranges reintroduced on

- Revenues between

$760 million and$775 million (raised from$755 million to$770 million ); - Net income between

$30 million and$34 million (raised from$23 million to$28 million ); - Adjusted EBITDA between

$166 million and$170 million (raised from$158 million to$163 million ); - Net cash provided by operating activities between

$132 million and$136 million (raised from$122 million to$126 million ); and - Adjusted Free Cash Flow between

$60 million and$64 million (raised from$53 million to$57 million ).

Adjusted EBITDA and Adjusted Free Cash Flow related to fiscal year 2020 are described in the Reconciliation of 2020 Outlook Non-GAAP Measures section of this press release. Net income and Net cash provided by operating activities are provided as the most directly comparable GAAP measures to Adjusted EBITDA and Adjusted Free Cash Flow, respectively however these forward-looking estimates for fiscal year 2020 do not contemplate any unanticipated impacts.

Presentation of Certain Non-GAAP Measures

Adjusted Diluted Earnings Per Common Share, Adjusted Net Income, Adjusted Operating

Income, Adjusted EBITDA, Adjusted Free Cash Flow, Bank Consolidated EBITDA,

Consolidated Funded Debt, Net and Consolidated Net Leverage Ratio are described

in the Reconciliation of Certain Non-GAAP Measures section of this document.

Non-GAAP measures are not in accordance with or an alternative for generally

accepted accounting principles in

Conference call to discuss quarter

The Company will host a conference call to discuss these results on

The call will also be webcast; to listen, participants should visit the company's website at http://ir.casella.com and follow the appropriate link to the webcast. A replay of the call will be available on the Company's website, or by calling (855) 859-2056 or (404) 537-3406 (Conference ID 246 1608).

About

Safe Harbor Statement

Certain matters discussed in this press release, including, but not limited to, the statements regarding our intentions, beliefs or current expectations concerning, among other things, the expected and potential direct or indirect impacts of the COVID-19 pandemic on our business; our financial performance; financial condition; operations and services; prospects; growth; strategies; and guidance for fiscal year 2020, are "forward-looking statements" intended to qualify for the safe harbors from liability established by the Private Securities Litigation Reform Act of 1995. These forward-looking statements can generally be identified as such by the context of the statements, including words such as "believe," "expect," "anticipate," "plan," "may," "would," "intend," "estimate," "will," "guidance" and other similar expressions, whether in the negative or affirmative. These forward-looking statements are based on current expectations, estimates, forecasts and projections about the industry and markets in which the Company operates and management's beliefs and assumptions. The Company cannot guarantee that it actually will achieve the financial results, plans, intentions, expectations or guidance disclosed in the forward-looking statements made. Such forward-looking statements, and all phases of the Company's operations, involve a number of risks and uncertainties, any one or more of which could cause actual results to differ materially from those described in its forward-looking statements.

Such risks and uncertainties include or relate to, among other things, the

following: it is challenging to predict the duration and severity of the COVID-19

pandemic and its negative effect on the economy, our operations and financial

results; policies adopted by

There are a number of other important risks and uncertainties that could cause

the Company's actual results to differ materially from those indicated by such

forward-looking statements. These additional risks and uncertainties include,

without limitation, those detailed in Item 1A, "Risk Factors" in the Company's

most recently filed Form 10-K and Form 10-Q and in other filings that the Company

may make with the

The Company undertakes no obligation to update publicly any forward-looking statements whether as a result of new information, future events or otherwise, except as required by law.

Investors:

Chief Financial Officer

(802) 772-2239

Media:

Vice President

(802) 772-2247

http://www.casella.com

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS

(Unaudited)

(In thousands, except for per share data)

| Three

Months Ended |

Nine

Months Ended |

||||||||||||||||||

| 2020 | 2019 | 2020 | 2019 | ||||||||||||||||

| Revenues | $ | 202,667 | $ | 198,547 | $ | 574,344 | $ | 549,670 | |||||||||||

| Operating expenses: | |||||||||||||||||||

| Cost of operations | 130,406 | 131,273 | 382,386 | 377,707 | |||||||||||||||

| General and administration | 25,014 | 22,536 | 74,240 | 67,423 | |||||||||||||||

| Depreciation and amortization | 23,799 | 20,940 | 67,281 | 58,144 | |||||||||||||||

| 2,642 | 625 | 3,815 | 2,097 | ||||||||||||||||

| Expense from acquisition activities | 173 | 1,097 | 1,533 | 2,237 | |||||||||||||||

| Withdrawal costs - multiemployer pension plan | — | 3,591 | — | 3,591 | |||||||||||||||

| 182,034 | 180,062 | 529,255 | 511,199 | ||||||||||||||||

| Operating income | 20,633 | 18,485 | 45,089 | 38,471 | |||||||||||||||

| Other expense (income): | |||||||||||||||||||

| Interest expense, net | 5,299 | 6,169 | 16,666 | 18,562 | |||||||||||||||

| Other income | (157 | ) | (248 | ) | (606 | ) | (960 | ) | |||||||||||

| Other expense, net | 5,142 | 5,921 | 16,060 | 17,602 | |||||||||||||||

| Income before income taxes | 15,491 | 12,564 | 29,029 | 20,869 | |||||||||||||||

| Provision (benefit) for income taxes | 374 | 178 | 840 | (1,718 | ) | ||||||||||||||

| Net income | $ | 15,117 | $ | 12,386 | $ | 28,189 | $ | 22,587 | |||||||||||

| Basic weighted average common shares outstanding | 48,370 | 47,690 | 48,241 | 47,029 | |||||||||||||||

| Basic earnings per common share | $ | 0.31 | $ | 0.26 | $ | 0.58 | $ | 0.48 | |||||||||||

| Diluted weighted average common shares outstanding | 48,619 | 48,361 | 48,481 | 47,660 | |||||||||||||||

| Diluted earnings per common share | $ | 0.31 | $ | 0.26 | $ | 0.58 | $ | 0.47 | |||||||||||

CONDENSED CONSOLIDATED BALANCE SHEETS

(In thousands)

2020 |

2019 |

||||||

| (Unaudited) | |||||||

| ASSETS | |||||||

| CURRENT ASSETS: | |||||||

| Cash and cash equivalents | $ | 21,127 | $ | 3,471 | |||

| Accounts receivable, net of allowance for credit losses | 73,604 | 80,205 | |||||

| Other current assets | 21,016 | 19,137 | |||||

| Total current assets | 115,747 | 102,813 | |||||

| Property, plant and equipment, net of accumulated depreciation and amortization | 492,022 | 443,825 | |||||

| Operating lease right-of-use assets | 101,433 | 108,025 | |||||

| 192,379 | 185,819 | ||||||

| Intangible assets, net of accumulated amortization | 59,390 | 58,721 | |||||

| Restricted assets | 1,619 | 1,586 | |||||

| Cost method investments | 11,264 | 11,264 | |||||

| Deferred income taxes | 7,390 | 8,577 | |||||

| Other non-current assets | 13,011 | 11,552 | |||||

| Total assets | $ | 994,255 | $ | 932,182 | |||

| LIABILITIES AND STOCKHOLDERS' EQUITY | |||||||

| CURRENT LIABILITIES: | |||||||

| Current maturities of debt | $ | 8,588 | $ | 4,301 | |||

| Current operating lease liabilities | 8,078 | 9,356 | |||||

| Accounts payable | 55,825 | 64,396 | |||||

| Other accrued liabilities | 65,058 | 52,536 | |||||

| Total current liabilities | 137,549 | 130,589 | |||||

| Debt, less current portion | 531,129 | 509,021 | |||||

| Operating lease liabilities, less current portion | 67,365 | 70,709 | |||||

| Other long-term liabilities | 110,225 | 99,110 | |||||

| Total stockholders' equity | 147,987 | 122,753 | |||||

| Total liabilities and stockholders' equity | $ | 994,255 | $ | 932,182 | |||

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(Unaudited)

(In thousands)

| Nine

Months Ended |

|||||||||

| 2020 | 2019 | ||||||||

| Cash Flows from Operating Activities: | |||||||||

| Net income | $ | 28,189 | $ | 22,587 | |||||

| Adjustments to reconcile net income to net cash provided by operating activities: | |||||||||

| Depreciation and amortization | 67,281 | 58,144 | |||||||

| Depletion of landfill operating lease obligations | 5,711 | 5,580 | |||||||

| Interest accretion on landfill and environmental remediation liabilities | 5,324 | 5,310 | |||||||

| Amortization of debt issuance costs | 1,597 | 1,724 | |||||||

| Stock-based compensation | 5,345 | 5,218 | |||||||

| Operating lease right-of-use assets expense | 6,636 | 7,272 | |||||||

| Loss (gain) on sale of property and equipment | 254 | (806 | ) | ||||||

| 2,077 | 58 | ||||||||

| Non-cash expense from acquisition activities | 549 | 71 | |||||||

| Withdrawal costs - multiemployer pension plan | — | 3,591 | |||||||

| Deferred income taxes | 1,514 | (1,267 | ) | ||||||

| Changes in assets and liabilities, net of effects of acquisitions and divestitures | (12,562 | ) | (35,987 | ) | |||||

| Net cash provided by operating activities | 111,915 | 71,495 | |||||||

| Cash Flows from Investing Activities: | |||||||||

| Acquisitions, net of cash acquired | (25,379 | ) | (73,496 | ) | |||||

| Additions to property, plant and equipment | (77,271 | ) | (75,998 | ) | |||||

| Proceeds from sale of property and equipment | 430 | 542 | |||||||

| Proceeds from property insurance settlement | — | 332 | |||||||

| Net cash used in investing activities | (102,220 | ) | (148,620 | ) | |||||

| Cash Flows from Financing Activities: | |||||||||

| Proceeds from debt borrowings | 154,400 | 121,500 | |||||||

| Principal payments on debt | (145,008 | ) | (149,774 | ) | |||||

| Payments of debt issuance costs | (1,531 | ) | — | ||||||

| Proceeds from the exercise of share based awards | 100 | 3,355 | |||||||

| Proceeds from the public offering of Class A Common Stock | — | 100,446 | |||||||

| Proceeds from unregistered sale of Class A Common Stock | — | 2,619 | |||||||

| Net cash provided by financing activities | 7,961 | 78,146 | |||||||

| Net increase in cash and cash equivalents | 17,656 | 1,021 | |||||||

| Cash and cash equivalents, beginning of period | 3,471 | 4,007 | |||||||

| Cash and cash equivalents, end of period | $ | 21,127 | $ | 5,028 | |||||

| Supplemental Disclosure of Cash Flow Information: | |||||||||

| Cash interest | $ | 15,239 | $ | 17,200 | |||||

| Cash income tax (refunds) payments | $ | (1,650 | ) | $ | 84 | ||||

| Supplemental Disclosure of Non-Cash Investing and Financing Activities: | |||||||||

| Non-current assets obtained through long-term obligations | $ | 16,937 | $ | 9,797 | |||||

RECONCILIATION OF CERTAIN NON-GAAP MEASURES

(Unaudited)

(In thousands)

Non-GAAP Performance Measures

In addition to disclosing financial results prepared in accordance with GAAP, the Company also presents non-GAAP performance measures such as Adjusted EBITDA, Adjusted Operating Income, Adjusted Net Income and Adjusted Diluted Earnings Per Common Share that provide an understanding of operational performance because it considers them important supplemental measures of the Company's performance that are frequently used by securities analysts, investors and other interested parties in the evaluation of the Company's results. The Company also believes that identifying the impact of certain items as adjustments provides more transparency and comparability across periods. Management uses these non-GAAP performance measures to further understand its "core operating performance" and believes its "core operating performance" is helpful in understanding its ongoing performance in the ordinary course of operations. The Company believes that providing such non-GAAP performance measures to investors, in addition to corresponding income statement measures, affords investors the benefit of viewing the Company's performance using the same financial metrics that the management team uses in making many key decisions and understanding how the core business and its results of operations has performed. The tables below set forth such performance measures on an adjusted basis to exclude such items:

| Three

Months Ended |

Nine

Months Ended |

||||||||||||||||||

| 2020 | 2019 | 2020 | 2019 | ||||||||||||||||

| Net income | $ | 15,117 | $ | 12,386 | $ | 28,189 | $ | 22,587 | |||||||||||

| Net income as a percentage of revenues | 7.5 | % | 6.2 | % | 4.9 | % | 4.1 | % | |||||||||||

| Provision (benefit) for income taxes | 374 | 178 | 840 | (1,718 | ) | ||||||||||||||

| Other income | (157 | ) | (248 | ) | (606 | ) | (960 | ) | |||||||||||

| Interest expense, net | 5,299 | 6,169 | 16,666 | 18,562 | |||||||||||||||

| Expense from acquisition activities (i) | 173 | 1,097 | 1,533 | 2,237 | |||||||||||||||

| 2,642 | 625 | 3,815 | 2,097 | ||||||||||||||||

| Withdrawal costs - multiemployer pension plan (iii) | — | 3,591 | — | 3,591 | |||||||||||||||

| Depreciation and amortization | 23,799 | 20,940 | 67,281 | 58,144 | |||||||||||||||

| Depletion of landfill operating lease obligations | 2,243 | 1,957 | 5,711 | 5,580 | |||||||||||||||

| Interest accretion on landfill and environmental remediation liabilities | 1,782 | 1,731 | 5,324 | 5,310 | |||||||||||||||

| Adjusted EBITDA | $ | 51,272 | $ | 48,426 | $ | 128,753 | $ | 115,430 | |||||||||||

| Adjusted EBITDA as a percentage of revenues | 25.3 | % | 24.4 | % | 22.4 | % | 21.0 | % | |||||||||||

| Depreciation and amortization | (23,799 | ) | (20,940 | ) | (67,281 | ) | (58,144 | ) | |||||||||||

| Depletion of landfill operating lease obligations | (2,243 | ) | (1,957 | ) | (5,711 | ) | (5,580 | ) | |||||||||||

| Interest accretion on landfill and environmental remediation liabilities | (1,782 | ) | (1,731 | ) | (5,324 | ) | (5,310 | ) | |||||||||||

| Adjusted Operating Income | $ | 23,448 | $ | 23,798 | $ | 50,437 | $ | 46,396 | |||||||||||

| Adjusted Operating Income as a percentage of revenues | 11.6 | % | 12.0 | % | 8.8 | % | 8.4 | % | |||||||||||

| Three

Months Ended |

Nine

Months Ended |

||||||||||||||||||

| 2020 | 2019 | 2020 | 2019 | ||||||||||||||||

| Net income | $ | 15,117 | $ | 12,386 | $ | 28,189 | $ | 22,587 | |||||||||||

| Expense from acquisition activities (i) | 173 | 1,097 | 1,533 | 2,237 | |||||||||||||||

| 2,642 | 625 | 3,815 | 2,097 | ||||||||||||||||

| Withdrawal costs - multiemployer pension plan (iii) | — | 3,591 | — | 3,591 | |||||||||||||||

| Tax effect (iv) | (4 | ) | 23 | (35 | ) | (67 | ) | ||||||||||||

| Adjusted Net Income | $ | 17,928 | $ | 17,722 | $ | 33,502 | $ | 30,445 | |||||||||||

| Diluted weighted average common shares outstanding | 48,619 | 48,361 | 48,481 | 47,660 | |||||||||||||||

| Diluted earnings per common share | $ | 0.31 | $ | 0.26 | $ | 0.58 | $ | 0.47 | |||||||||||

| Expense from acquisition activities (i) | — | 0.02 | 0.03 | 0.05 | |||||||||||||||

| 0.06 | 0.01 | 0.08 | 0.04 | ||||||||||||||||

| Withdrawal costs - multiemployer pension plan (iii) | — | 0.08 | — | 0.08 | |||||||||||||||

| Adjusted Diluted Earnings Per Common Share | $ | 0.37 | $ | 0.37 | $ | 0.69 | $ | 0.64 | |||||||||||

?(i) Expense from acquisition activities are primarily legal, consulting or other similar costs incurred during the period related to acquisition diligence, acquisition integration or select development projects as part of the Company's strategic growth initiative.

(ii)

(iii) Withdrawal costs — multiemployer pension plan consists of a charge related to withdrawal from a multiemployer pension plan.

(iv) Tax effect of the adjustments is an aggregate of the current and deferred tax impact of each adjustment, including the impact to the effective tax rate, current provision and deferred provision. The computation considers all relevant impacts of the adjustments, including available net operating loss carryforwards and the impact on the valuation allowance.

Non-GAAP Liquidity Measures

In addition to disclosing financial results prepared in accordance with GAAP, the Company also presents non-GAAP liquidity measures such as Adjusted Free Cash Flow, Bank Consolidated EBITDA, Consolidated Funded Debt, Net and Consolidated Net Leverage Ratio that provide an understanding of the Company's liquidity because it considers them important supplemental measures of its liquidity that are frequently used by securities analysts, investors and other interested parties in the evaluation of the Company's cash flow generation from its core operations that are then available to be deployed for strategic acquisitions, growth investments, development projects, unusual landfill closures, site improvement and remediation, and strengthening the Company's balance sheet through paying down debt. The Company also believes that identifying the impact of certain items as adjustments provides more transparency and comparability across periods. Management uses non-GAAP liquidity measures to understand the Company's cash flow provided by operating activities after certain expenditures along with its consolidated net leverage and believes that these measures demonstrate the Company's ability to execute on its strategic initiatives. The Company believes that providing such non-GAAP liquidity measures to investors, in addition to corresponding cash flow statement measures, affords investors the benefit of viewing the Company's liquidity using the same financial metrics that the management team uses in making many key decisions and understanding how the core business and cash flow generation has performed. The tables below, in some instances on an adjusted basis to exclude certain items, set forth such liquidity measures:

| Three

Months Ended |

Nine

Months Ended |

||||||||||||||||||

| 2020 | 2019 | 2020 | 2019 | ||||||||||||||||

| Net cash provided by operating activities | $ | 49,422 | $ | 33,244 | $ | 111,915 | $ | 71,495 | |||||||||||

| Capital expenditures | (25,701 | ) | (29,339 | ) | (77,271 | ) | (75,998 | ) | |||||||||||

| Proceeds from sale of property and equipment | 230 | 179 | 430 | 542 | |||||||||||||||

| Proceeds from property insurance settlement | — | 332 | — | 332 | |||||||||||||||

| 1,979 | 4,863 | 4,737 | 11,083 | ||||||||||||||||

| Cash outlays from acquisition activities (ii) | 199 | 957 | 984 | 2,166 | |||||||||||||||

| Post acquisition and development project capital expenditures (iii) | 3,235 | 5,882 | 12,510 | 11,912 | |||||||||||||||

| 3,154 | 2,570 | 6,700 | 2,570 | ||||||||||||||||

| Adjusted Free Cash Flow | $ | 32,518 | $ | 18,688 | $ | 60,005 | $ | 24,102 | |||||||||||

(i)

(ii) Cash outlays from acquisition activities are cash outlays for transaction and integration costs relating to specific acquisition transactions and include legal, environmental, valuation and consulting as well as asset, workforce and system integration costs as part of the Company's strategic growth initiative.

(iii) Post acquisition and development project capital expenditures are (x) acquisition related capital expenditures that are necessary to optimize strategic synergies associated with integrating newly acquired operations as contemplated by the discounted cash flow return analysis conducted by management as part of the acquisition investment decision; and (y) non-routine development investments that are expected to provide long-term returns. Acquisition related capital expenditures include the following costs required to achieve initial operating synergies: trucks, equipment and machinery; and facilities, land, IT infrastructure or related upgrades to integrate operations.

(iv)

Following is the Consolidated Net Leverage Ratio and the reconciliations of Consolidated Funded Debt, Net from debt and Bank Consolidated EBITDA from Net cash provided by operating activities:

| Twelve

Months Ended |

Covenant

Requirement at |

||||

| Consolidated Net Leverage Ratio (i) | 2.99 | 4.00 | |||

(i) Our credit agreement requires us to maintain a maximum consolidated net leverage ratio, to be measured at the end of each fiscal quarter ("Consolidated Net Leverage Ratio"). The Consolidated Net Leverage Ratio is calculated as consolidated debt, net of unencumbered cash and cash equivalents in excess of

| Twelve

Months Ended |

||||

| Net cash provided by operating activities | $ | 157,249 | ||

| Changes in assets and liabilities, net of effects of acquisitions and divestitures | 5,184 | |||

| Loss on sale of property and equipment | (168 | ) | ||

| Non-cash expense from acquisition activities | (543 | ) | ||

| Withdrawal costs - multiemployer pension plan | 1,361 | |||

| (2,093 | ) | |||

| Operating lease right-of-use assets expense | (8,923 | ) | ||

| Stock-based compensation | (7,350 | ) | ||

| Interest expense, less amortization of debt issuance costs | 20,956 | |||

| Benefit for income taxes, net of deferred income taxes | (853 | ) | ||

| Adjustments as allowed by the credit agreement | 12,659 | |||

| Bank Consolidated EBITDA | $ | 177,479 | ||

RECONCILIATION OF 2020 OUTLOOK NON-GAAP MEASURES

(Unaudited)

(In thousands)

Following is a reconciliation of the Company's estimated Adjusted EBITDA (i) from estimated Net income for the fiscal year ending

| (Estimated)

Fiscal Year Ending |

||

| Net income | ||

| Provision for income taxes | 1,000 | |

| Other income | (800) | |

| Interest expense, net | 23,000 | |

| Expense from acquisition activities | 1,800 | |

| 4,500 | ||

| Depreciation and amortization | 92,000 | |

| Depletion of landfill operating lease obligations | 7,500 | |

| Interest accretion on landfill and environmental remediation liabilities | 7,000 | |

| Adjusted EBITDA | ||

Following is a reconciliation of the Company's estimated Adjusted Free Cash Flow (i) from estimated Net cash provided by operating activities for the fiscal year ending

| (Estimated)

Fiscal Year Ending |

||

| Net cash provided by operating activities | ||

| Capital expenditures | (113,000) | |

| Proceeds from sale of property and equipment | 500 | |

| 8,000 | ||

| Cash outlays from acquisition activities | 1,000 | |

| Post acquisition and development project capital expenditures | 18,000 | |

| 13,500 | ||

| Adjusted Free Cash Flow | ||

(i) See footnotes for Non-GAAP Performance Measures and Non-GAAP Liquidity Measures included in the Reconciliation of Certain Non-GAAP Measures for further disclosure over the nature of the various adjustments to estimated Adjusted EBITDA and estimated Adjusted Free Cash Flow.

SUPPLEMENTAL DATA TABLES

(Unaudited)

(In thousands)

Amounts of total revenues attributable to services provided for the three and nine months ended

| Three

Months Ended |

|||||||||||||

| 2020 | %

of Total Revenues |

2019 | %

of Total Revenues |

||||||||||

| Collection | $ | 102,270 | 50.5 | % | $ | 98,966 | 49.8 | % | |||||

| Disposal | 47,600 | 23.5 | % | 50,552 | 25.5 | % | |||||||

| Power generation | 987 | 0.5 | % | 808 | 0.4 | % | |||||||

| Processing | 2,194 | 1.0 | % | 2,640 | 1.3 | % | |||||||

| Solid waste operations | 153,051 | 75.5 | % | 152,966 | 77.0 | % | |||||||

| Organics | 14,539 | 7.2 | % | 14,166 | 7.2 | % | |||||||

| Customer solutions | 22,320 | 11.0 | % | 20,689 | 10.4 | % | |||||||

| Recycling | 12,757 | 6.3 | % | 10,726 | 5.4 | % | |||||||

| Resource solutions operations | 49,616 | 24.5 | % | 45,581 | 23.0 | % | |||||||

| Total revenues | $ | 202,667 | 100.0 | % | $ | 198,547 | 100.0 | % | |||||

| Nine

Months Ended |

|||||||||||||

| 2020 | %

of Total Revenues |

2019 | %

of Total Revenues |

||||||||||

| Collection | $ | 290,837 | 50.6 | % | $ | 274,111 | 49.9 | % | |||||

| Disposal | 129,971 | 22.6 | % | 134,746 | 24.5 | % | |||||||

| Power generation | 2,931 | 0.5 | % | 2,655 | 0.5 | % | |||||||

| Processing | 5,281 | 1.0 | % | 5,426 | 1.0 | % | |||||||

| Solid waste operations | 429,020 | 74.7 | % | 416,938 | 75.9 | % | |||||||

| Organics | 44,890 | 7.8 | % | 42,668 | 7.7 | % | |||||||

| Customer solutions | 64,223 | 11.2 | % | 58,058 | 10.6 | % | |||||||

| Recycling | 36,211 | 6.3 | % | 32,006 | 5.8 | % | |||||||

| Resource solutions operations | 145,324 | 25.3 | % | 132,732 | 24.1 | % | |||||||

| Total revenues | $ | 574,344 | 100.0 | % | $ | 549,670 | 100.0 | % | |||||

Components of revenue growth for the three months ended

| Amount | %

of Related Business |

%

of Operations |

%

of Total Company |

||||||||||||

| Solid waste operations: | |||||||||||||||

| Collection | $ | 3,672 | 3.7 | % | 2.4 | % | 1.8 | % | |||||||

| Disposal | 2,421 | 4.8 | % | 1.6 | % | 1.3 | % | ||||||||

| Processing | — | — | % | — | % | — | % | ||||||||

| Solid waste price | 6,093 | 8.5 | % | 4.0 | % | 3.1 | % | ||||||||

| Collection | (6,340 | ) | (4.1 | ) | % | (3.2 | ) | % | |||||||

| Disposal | (6,171 | ) | (4.0 | ) | % | (3.1 | ) | % | |||||||

| Processing | (301 | ) | (0.3 | ) | % | (0.2 | ) | % | |||||||

| Solid waste volume | (12,812 | ) | (8.4 | ) | % | (6.5 | ) | % | |||||||

| Fuel surcharge and other fees | (253 | ) | (0.1 | ) | % | (0.1 | ) | % | |||||||

| Commodity price and volume | 36 | — | % | — | % | ||||||||||

| Acquisitions, net divestitures | 7,020 | 4.6 | % | 3.5 | % | ||||||||||

| Closed operations | 1 | — | % | — | % | ||||||||||

| Total solid waste operations | 85 | 0.1 | % | — | % | ||||||||||

| Resource solutions operations: | |||||||||||||||

| Organics | 373 | 0.8 | % | 0.2 | % | ||||||||||

| Customer solutions | 1,631 | 3.6 | % | 0.9 | % | ||||||||||

| Recycling: | |||||||||||||||

| Commodity price | 1,187 | 11.1 | % | 2.6 | % | 0.6 | % | ||||||||

| Processing price | 12 | 0.1 | % | — | % | — | % | ||||||||

| Volume | 521 | 4.9 | % | 1.1 | % | 0.3 | % | ||||||||

| Commodity acquisition | 311 | 2.8 | % | 0.8 | % | 0.1 | % | ||||||||

| Recycling | 2,031 | 18.9 | % | 4.5 | % | 1.0 | % | ||||||||

| Total resource solutions operations | 4,035 | 8.9 | % | 2.1 | % | ||||||||||

| Total company | $ | 4,120 | 2.1 | % | |||||||||||

Solid waste internalization rates by region for the three and nine months ended

| Three

Months Ended |

Nine

Months Ended |

||||||||||

| 2020 | 2019 | 2020 | 2019 | ||||||||

| Eastern region | 47.3 | % | 51.9 | % | 47.8 | % | 49.8 | % | |||

| Western region | 61.4 | % | 63.0 | % | 61.3 | % | 61.3 | % | |||

| Solid waste internalization | 54.9 | % | 57.4 | % | 54.9 | % | 55.3 | % | |||

Components of capital expenditures (i) for the three and nine months ended

| Three

Months Ended |

Nine

Months Ended |

||||||||||||||

| 2020 | 2019 | 2020 | 2019 | ||||||||||||

| Growth capital expenditures: | |||||||||||||||

| Post acquisition and development project | $ | 3,235 | $ | 5,882 | $ | 12,510 | $ | 11,912 | |||||||

| 3,154 | 2,570 | 6,700 | 2,570 | ||||||||||||

| Other | 930 | 635 | 1,910 | 1,523 | |||||||||||

| Growth capital expenditures | 7,319 | 9,087 | 21,120 | 16,005 | |||||||||||

| Replacement capital expenditures: | |||||||||||||||

| Landfill development | 10,100 | 7,225 | 29,920 | 21,278 | |||||||||||

| Vehicles, machinery, equipment and containers | 6,455 | 11,045 | 20,824 | 33,961 | |||||||||||

| Facilities | 995 | 1,257 | 2,559 | 3,375 | |||||||||||

| Other | 832 | 725 | 2,848 | 1,379 | |||||||||||

| Replacement capital expenditures | 18,382 | 20,252 | 56,151 | 59,993 | |||||||||||

| Capital expenditures | $ | 25,701 | $ | 29,339 | $ | 77,271 | $ | 75,998 | |||||||

(i) The Company's capital expenditures are broadly defined as pertaining to either growth or replacement activities. Growth capital expenditures are defined as costs related to development projects, organic business growth, and the integration of newly acquired operations. Growth capital expenditures include costs related to the following: 1) post acquisition and development projects that are necessary to optimize strategic synergies associated with integrating newly acquired operations as contemplated by the discounted cash flow return analysis conducted by management as part of the acquisition investment decision as well as non-routine development investments that are expected to provide long-term returns and includes the following capital expenditures required to achieve initial operating synergies: trucks, equipment and machinery; and facilities, land, IT infrastructure or related upgrades to integrate operations; 2)

Source: Casella Waste Systems, Inc.

Sign up to receive our free Weekly News Bulletin